")

Many first-time business owners focus heavily on branding, marketing, and sales while bookkeeping becomes an afterthought. However, clean and organized financial records are essential for tracking growth, managing expenses, securing funding, and filing taxes correctly.

Preparing your books doesn’t require you to be an accountant but it does require discipline, the right systems, and an understanding of financial basics. Many growing businesses also choose to Outsource Bookkeeping Services to experienced professionals who ensure accuracy and efficiency in financial management.

Why Proper Bookkeeping Matters for New Business Owners

Bookkeeping is more than just recording income and expenses. It directly impacts your business stability and growth potential. Many Bookkeeping Firms help businesses maintain structured financial records and avoid costly financial mistakes.

1. Helps You Understand Cash Flow

Cash flow is the lifeline of any new business. Even profitable companies can fail if they run out of cash. Accurate books help you monitor incoming revenue, outgoing expenses, and available working capital.

2. Ensures Tax Compliance

Incorrect or incomplete financial records can lead to penalties, audits, and unnecessary stress. Organized books simplify tax filing and ensure you claim eligible deductions.

3. Supports Better Decision-Making

When you know your revenue trends, profit margins, and expense breakdowns, you can make informed decisions about hiring, pricing, expansion, and investments.

4. Builds Credibility with Investors and Banks

If you ever seek funding or loans, lenders will request financial statements. Well-prepared books demonstrate professionalism and financial discipline.

5. Prevents Costly Mistakes

Mixing personal and business finances, missing invoices, or ignoring reconciliations can create financial confusion. Proper bookkeeping reduces errors and financial blind spots. Many startups prefer Bookkeeping Outsource Services to ensure that their financial data remains accurate from the beginning.

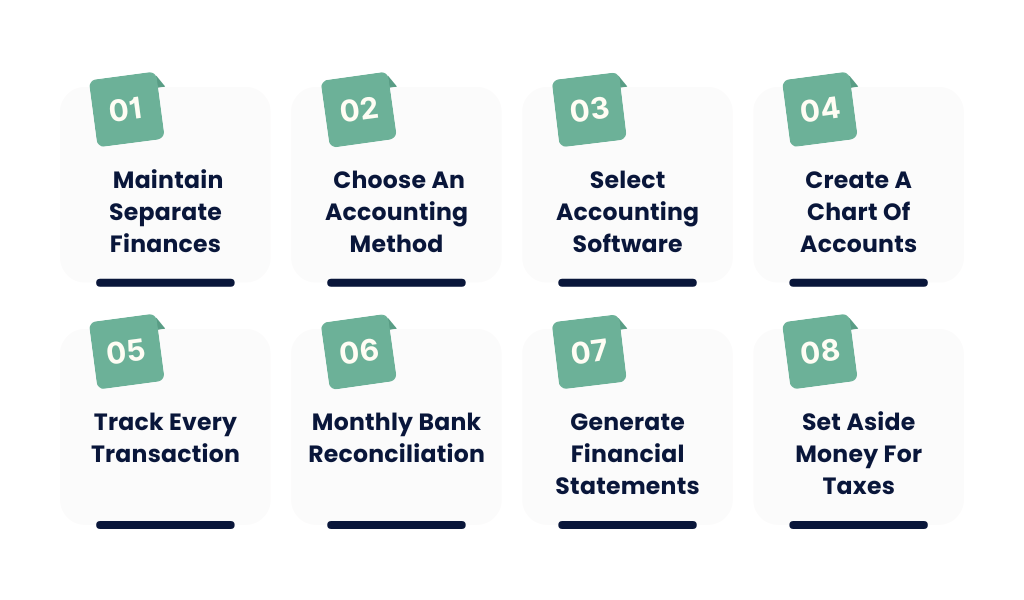

Step-by-Step Guide to Setting Up Your Business Books

Here’s a practical roadmap to prepare your books correctly as a first-time business owner:

Step 1: Maintain Separate Finances

Open a dedicated business bank account and credit card. Never mix personal and business transactions. This simplifies tracking and protects you legally.

Step 2: Choose an Accounting Method

You generally have two options:

- Cash Basis Accounting – Record income when you receive payment and expenses when you pay them.

- Accrual Accounting – Record income when earned and expenses when incurred.

Most small businesses start with a cash basis for simplicity, but growing businesses may benefit from accrual accounting for better financial visibility.

Step 3: Select Accounting Software

Manual spreadsheets can work temporarily, but accounting software is more reliable and efficient. Popular options include:

- QuickBooks

- Xero

- Zoho Books

These platforms help automate invoicing, expense tracking, reconciliation, and financial reporting. Many companies offering Bookkeeping USA services rely on these tools to manage client accounts efficiently.

Step 4: Create a Chart of Accounts

A Chart of Accounts is a categorized list of all financial transactions in your business. It typically includes:

- Income

- Cost of Goods Sold (COGS)

- Operating Expenses

- Assets

- Liabilities

- Equity

This structure keeps your financial records organized and easy to interpret.

Step 5: Track Every Transaction

Record all income and expenses consistently. This includes:

- Sales revenue

- Vendor payments

- Utility bills

- Marketing expenses

- Travel costs

- Subscription fees

Keep digital copies of receipts and invoices. Many Accounting Tools allow you to upload and store them directly.

Step 6: Monthly Bank Reconciliation

Reconciliation means matching your recorded transactions with your bank statements. Doing this monthly helps identify errors, missing entries, or fraudulent activity.

Step 7: Generate Financial Statements

At minimum, review these reports regularly:

- Profit & Loss Statement (Income Statement) – Shows profitability.

- Balance Sheet – Displays assets and liabilities.

- Cash Flow Statement – Tracks money movement.

These reports provide clarity on your financial health.

Step 8: Set Aside Money for Taxes

First-time business owners often forget to reserve funds for taxes. Estimate your tax liability and transfer a percentage of profits into a separate savings account regularly.

Common Mistakes First-Time Business Owners Make

Avoid these frequent bookkeeping errors:

1. Mixing Personal and Business Expenses

This creates accounting confusion and potential legal complications.

2. Ignoring Small Transactions

Small expenses add up and can significantly impact your profitability and tax deductions.

3. Not Reconciling Accounts Regularly

Delaying reconciliation can lead to large discrepancies that are harder to fix later.

4. Failing to Keep Receipts

Without documentation, you may lose valid tax deductions.

5. Waiting Until Tax Season

Trying to organize an entire year’s records at once is stressful and increases the risk of mistakes.

6. Not Understanding Basic Financial Reports

Many new business owners avoid reviewing reports because they seem complex. However, basic financial literacy is essential for growth.

When to Hire a Professional Bookkeeper

While many first-time business owners start by managing their own books, there comes a point when professional help becomes necessary.

Consider hiring a bookkeeper if:

- Your transactions are increasing rapidly.

- You struggle to keep records updated.

- You’re unsure about tax compliance.

- You need financial forecasting.

- You plan to apply for funding or loans.

- You want to focus more on growing your business than managing paperwork.

A professional bookkeeper ensures accuracy, reduces risk, and saves time allowing you to focus on strategy and operations.

Outsourcing Bookkeeping can also be cost-effective compared to hiring a full-time in-house accountant.

Conclusion

Preparing your books as a first-time business owner may seem intimidating but it doesn’t have to be. With the right systems, consistent tracking, and financial awareness, you can build a strong foundation for long-term success.

Start by separating finances, choosing the right Accounting method, using reliable software, and maintaining regular reconciliation. Avoid common mistakes and don’t hesitate to seek professional help when needed.

Remember: bookkeeping isn’t just about compliance it’s about clarity, control, and confidence in your business journey.

Strong books today mean smarter growth tomorrow.

FAQs

1. What is the easiest accounting method for a first-time business owner?

Cash basis accounting is usually the simplest method because it records income and expenses only when money changes hands.

2. Do I need accounting software as a new business owner?

While spreadsheets can work initially, Accounting Software provides automation, accuracy, and better reporting. It becomes essential as your business grows.

3. How often should I update my books?

Ideally, transactions should be recorded weekly, and accounts should be reconciled monthly to maintain accuracy.

4. What financial reports should I review regularly?

You should review your Profit & Loss Statement, Balance Sheet, and Cash Flow Statement at least monthly.

5. Can I manage bookkeeping myself?

Yes, many first-time business owners start independently. However, as complexity increases, hiring a professional bookkeeper is recommended.

6. What happens if my books are not accurate?

Inaccurate books can lead to tax penalties, poor financial decisions, cash flow issues, and difficulty securing funding.

7. When is the right time to outsource bookkeeping?

The right time is when Bookkeeping starts consuming too much of your time, becomes confusing, or begins affecting your business growth.