The contemporary digital-first environment demands that accounting firms establish financial data protection systems, which have become essential for their operational success. USA Accounting Firms need to develop proactive data security measures because of rising cyber threats and growing regulatory demands and increasing client security requirements.

Accounting firms handle highly sensitive information such as tax records, Social Security numbers, payroll data, and financial statements. This combination of factors makes them an attractive target for cybercriminals.

The guide provides USA accounting firms with contemporary cybersecurity methods to protect financial information and shows them how to implement compliance frameworks and develop operational strategies.

Why Financial Data Protection Matters for USA Accounting Firms

The implications for financial data breaches include:

- Monetary damages and ransomware payments

- Penalties as per the USA laws

- Destruction of customer confidence and reputational harm

Indeed, financial organizations incur some of the most expensive data breaches at an average cost of more than $6 million per breach.

Moreover, some of the regulatory requirements that USA Accounting Firms have to adhere to include:

- Safeguards Rule by the FTC

- GLBA (Gramm-Leach-Bliley Act)

- SOX (Sarbanes-Oxley Act)

- Publication 4557 (Guidelines on Data Security) by IRS

Top Cybersecurity Threats Facing Accounting Firms

Prior to the implementation of solutions, it is vital to consider the risks involved.

1. Phishing and Email Attacks

Hackers disguise themselves as customers or even IRS agents to gain usernames and passwords.

2. Ransomware Attacks

Hacker groups block your system until you pay a ransom for recovery. The cost could be more than millions of dollars.

3. Insiders

Employees with too much access could either unintentionally or intentionally release information.

4. Lack of Cloud Security Measures

Cloud systems that are not properly configured are vulnerable to releasing financial data.

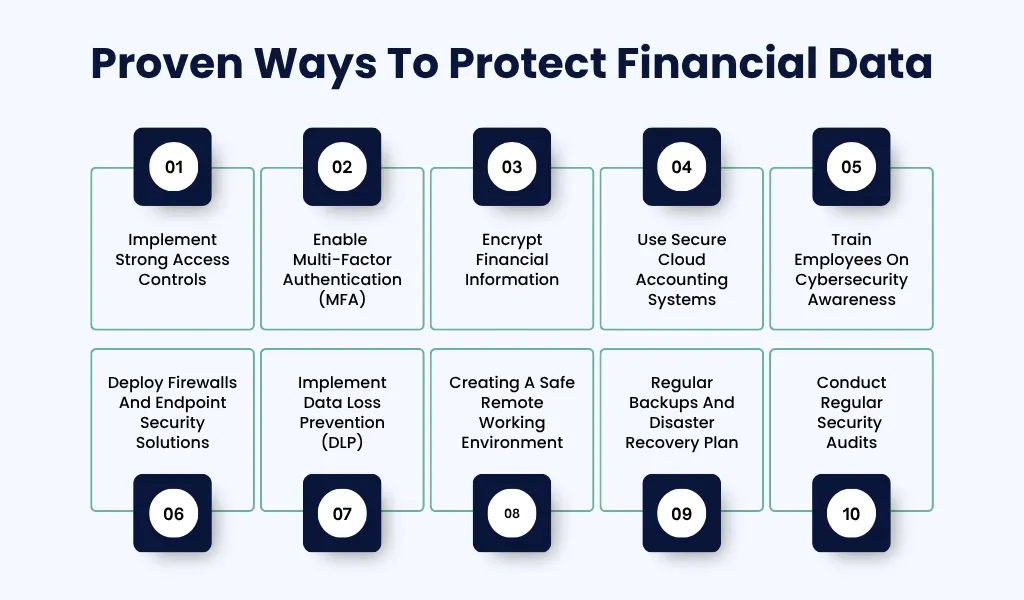

10 Proven Ways to Protect Financial Data

1. Implement Strong Access Controls

It is not necessary for all employees to have access to all financial information.

- Implement role-based access control (RBAC).

- Limit access to sensitive information to only authorized individuals.

- Conduct regular audits of access logs.

This helps reduce the risk of any security breaches from within the organization.

2. Enable Multi-Factor Authentication (MFA)

A password alone is insufficient for security.

- Apply multi-factor authentication to accounting software, email, and cloud storage

- Include biometric or one-time password (OTP) verification

Multi-factor authentication greatly minimizes the possibility of data breaches.

3. Encrypt Financial Information

Encryption guarantees that even if data is stolen, it will not be useful.

- Encrypt both stored and transmitted data

- Use reputable cloud service providers with encryption capabilities

Contemporary accounting applications must have integrated encryption options.

4. Use Secure Cloud Accounting Systems

It is quite prevalent in the USA, although security needs to be taken into consideration.

Key steps include:

- SOC 2 compliant applications

- Encryption keys managed by customers

- Monitoring API access and cloud endpoints

Improper cloud configurations have caused many breaches.

5. Train Employees on Cybersecurity Awareness

Human mistakes pose a significant threat.

Educate your employees on how to:

- Detect phishing emails

- Create secure passwords.

- Safely share files

Organizations frequently perform phishing simulations to raise awareness about the issue.

6. Deploy Firewalls and Endpoint Security Solutions

Traditional security measures should not be overlooked.

- Install firewalls to filter out unwanted traffic.

- Use antivirus and anti-malware programs.

- Endpoint security for remote devices

Software updates are essential to fend off cyber threats.

7. Implement Data Loss Prevention (DLP)

DLP technologies track and manage the distribution of sensitive information.

They do this by:

- Identifying any unauthorized transfer of files

- Stopping any leakages through emails or USB drives

- Monitoring sensitive financial transactions

This is particularly significant when dealing with several clients within a CPA Firm.

8. Creating a Safe Remote Working Environment

Working remotely exposes businesses to more risks.

Recommendations include:

- Implementing virtual private networks for secure connections

- Ensuring access to devices from the company only

- Enabling remote wiping on lost devices

The physical protection of devices is equally vital.

9. Regular Backups and Disaster Recovery Plan

Always be prepared for the worst.

- Take daily automated backups

- Secure backups offline or in the cloud

- Test your restoration process on a regular basis

This will help you maintain business continuity even after a cyber attack.

10. Conduct Regular Security Audits

Cybersecurity is not a one-time effort.

- Perform penetration testing

- Audit systems and processes

- Identify vulnerabilities and fix them proactively

Continuous monitoring helps stay ahead of evolving threats.

Compliance Requirements for USA Accounting Firms

In order to safeguard financial data, companies need to be in accordance with U.S. compliance requirements.

Major Regulations:

- FTC Safeguard Rule – Security program for consumer data

- Gramm-Leach-Bliley Act – Financial privacy

- IRS Requirements – Protection of taxpayer data

- SOC 2 Compliance – Secure service delivery

Compliance not only makes you comply with the law; it also enhances client trust.

Building a Data Security Framework for Your Firm

Data protection must encompass:

1. Risk Assessment

Determine any weaknesses in the system, process, and personnel.

2. Security Policies

Establish guidelines for accessing, storing and exchanging information.

3. Technical Infrastructure

Implement safe accounting software, firewall systems, and monitoring systems.

4. Incident Response Plan

Develop an incident response plan for data breaches.

Future Trends in Accounting Data Security

Cybersecurity is changing at an accelerated pace. American accounting companies need to be ready for the following:

1. AI-Based Threat Identification

AI can detect any abnormal behavior.

2. Zero-Trust Security Frameworks

Each and every access attempt will be scrutinized.

3. Cutting-Edge Encryption Techniques

Including quantum-proof encryption.

4. Higher Regulatory Scrutiny

With even more rigorous regulations in the next few years.

Conclusion

Financial data protection within Accounting Firms goes beyond just implementing technology; it requires the creation of a security culture.

USA accounting firms that spend on cybersecurity solutions:

- Enhance client confidence

- Safeguard themselves from losses.

- Maintain regulatory compliance

- Get ahead of the competition

Given the increasing frequency of cyberattacks and the attractiveness of financial data to hackers, it is not a matter of whether an accounting firm will encounter a security problem but rather when.

The ones who come out victorious are those that are ready for anything.

FAQs

1. How can financial data be protected effectively in accounting firms?

The best methods that ensure financial data protection in Accounting Firms are multifactor authentication (MFA), encryption, cloud protection, and security audits. The following regulations need to be implemented in USA accounting firms: the FTC Safeguards Rule and IRS data security regulations.

2. Why would cybercriminals be interested in targeting accounting firms?

Accounting firms provide a wealth of information, including SSN numbers, financial records, and tax data that could be used for identity theft or fraud.

3. What cybersecurity rules and regulations apply to accounting firms in the United States?

Some of the important regulations are the following:

- FTC Safeguards Rule

- Gramm-Leach-Bliley Act (GLBA)

- IRS Publication 4557

- Sarbanes-Oxley Act (SOX)

These rules and regulations require firms to provide strict data protection and privacy.

4. How does encryption help protect financial data from cybercrimes?

The process of encryption involves conversion of sensitive financial data to cipher text, which means hackers will not be able to decode it if they manage to break into an accounting firm’s systems.

5. What is MFA, and why is it necessary for accounting firms?

MFA refers to authentication using more than one factor. It improves security by requiring users to provide two factors, for example, a password and a one-time verification code. It significantly limits the possibility of any hacking attempts.

6. How can accounting firms protect themselves from phishing attacks?

Accounting firms can avoid phishing attacks by doing the following:

- Educating staff on phishing tactics

- Installing filters for email messages

- Verifying clients’ requests before disclosing confidential information

Periodic cybersecurity training is vital in avoiding mistakes made by staff members.

7. How frequently should accounting firms undertake security audits?

Security Audits should be conducted yearly. Other tasks like monitoring and vulnerability testing can take place periodically throughout the year. In some instances, accounting firms need quarterly security audits due to high risks.