The majority of businesses and individuals work to meet tax requirements. However, certain patterns and inconsistencies in their operations create hidden tax compliance risks, which can alert the IRS about their activities, such as discrepancies in reported income or unusual deductions that deviate from industry norms. An Audit isn’t always random; in many cases, it’s triggered by specific risk indicators in your tax return.

The detection of audit red flags enables you to take preventive action, which decreases risk and maintains authentic and precise financial statements. The following list contains main triggers that attract IRS focus along with methods to prevent their occurrence.

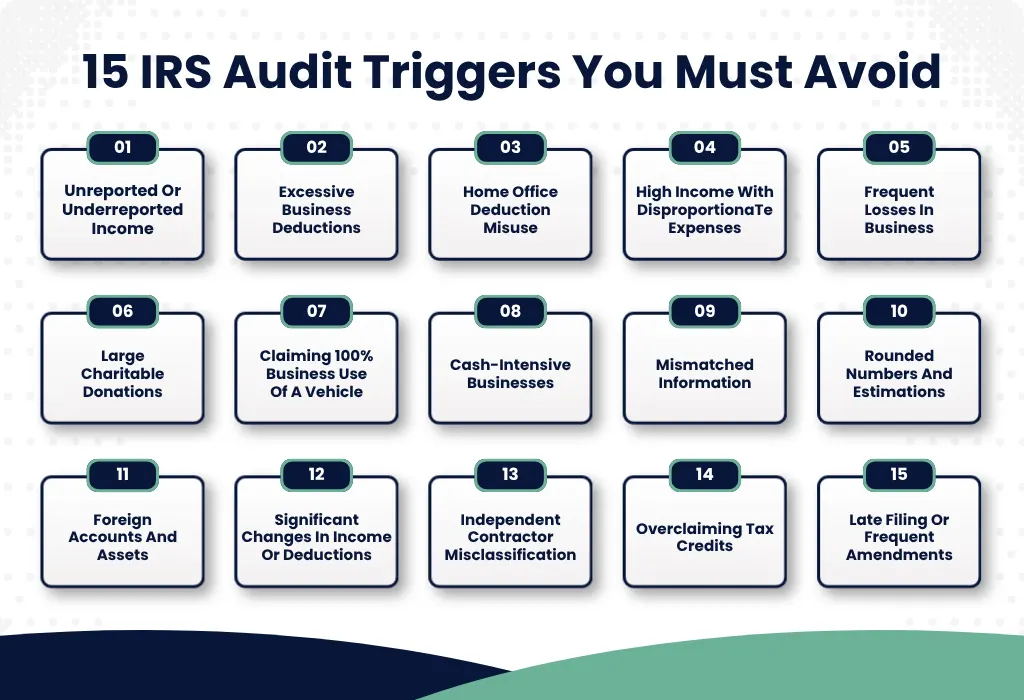

Avoid These 15 Common IRS Audit Triggers in 2026

1. Unreported or Underreported Income

One of the biggest audit triggers is failing to report all sources of income. Your income statements, which include W-2s and 1099s, are sent to the IRS, who uses automated systems to match these documents with your tax return.

Red flag examples:

- Missing freelance or side income

- Not reporting cash payments

- Forgetting investment or rental income

How to avoid it:

All income should be matched to official documents, and all income sources, including minor and irregular earnings, should be documented.

2. Excessive Business Deductions

Though deductions will lower your taxable income, having deductions that are unusually high relative to your income may invite an audit.

Risky deductions include the following:

- Traveling and entertainment costs

- Office expenses and equipment

- Consultation and marketing costs

Avoid it by:

Ensuring all deductions have appropriate justification for their necessity.

3. Home Office Deduction Misuse

The home office deduction is legitimate; however, it is frequently abused, thus becoming a popular item for audits.

Signs of fraud may be:

- Using private space (such as a bedroom) as a home office

- Exaggerating the portion of the house used for work

- A lack of exclusivity and consistency

Ways to prevent being audited on a home office:

- Use only those rooms that have strictly business purposes.

4. High Income with Disproportionate Expenses

If you have a high income but low business profits because of high costs, it might be an issue.

Why is it important?

The IRS may think that your business is not real and that you’re using it to cover up for personal expenses.

How can you prevent this from happening?

Keep your personal and business expenses separate, and make sure they fit with what your industry typically spends.

5. Frequent Losses in Business

Consistent losses from year to year may suggest that your enterprise is more of a hobby than an income-producing venture.

Danger signal example:

- Losses for many consecutive years

- Lack of a viable plan for turning a profit

How to prevent this problem:

- Show a sincere desire to earn a profit through sound business practices and planning.

6. Large Charitable Donations

Although generosity is promoted, very high donations in relation to your salary may cause scrutiny.

Common Problems:

- Appraisal of donations at too high a value

- Inadequate paperwork for the transaction

How to Avoid It:

- Make sure that all donations are recorded accurately, particularly those that do not involve cash.

7. Claiming 100% Business Use of a Vehicle

It is uncommon to state that a vehicle is solely utilized for business uses. It raises red flags when there is:

- No personal mileage indicated

- Absence of a mileage log

To steer clear of this situation:

- Keep a thorough mileage log and properly allocate business and personal miles.

8. Cash-Intensive Businesses

Firms that rely heavily on cash payments, such as restaurants, hair salons, or other small businesses, are subject to audits because they pose a higher risk of tax fraud.

Why it’s important:

Cash transactions can be easily manipulated; thus, the Internal Revenue Service concentrates on them.

How to prevent it:

Establish internal controls and keep a log of all cash transactions.

9. Mismatched Information

Differences between your tax return and third-party information will automatically be flagged by the IRS system.

Examples:

- Your clients’ income does not match the amount on your return.

- Social Security numbers and names are incorrectly entered.

How to prevent it:

- Make sure that all information is correct before submitting your return.

10. Rounded Numbers and Estimations

Use of rounded figures such as $5,000 or $10,000, rather than exact figures, can be an indicator of approximate or falsified data.

Why this is important:

This indicates poor record-keeping practices.

What can you do to prevent this?

Always use precise figures drawn from real financial data.

11. Foreign Accounts and Assets

The failure to report foreign bank accounts and foreign income is a big warning sign and could result in serious consequences.

Triggers:

- Failing to file international information returns

- Foreign income that isn’t reported

Prevention strategies:

- Always comply with the regulations concerning foreign property.

12. Significant Changes in Income or Deductions

A sudden spike or drop in income or deductions compared to previous years can attract attention.

Red flag scenario:

- Drastic increase in expenses without clear explanation

- Sudden drop in revenue

How to avoid it:

Be prepared to explain major changes with supporting documentation.

13. Independent Contractor Misclassification

Employee Misclassification As Independent Contractors To Reduce Taxes

Why It Matters:

The IRS keeps close tabs on worker classifications to ensure that proper taxes are paid.

How To Avoid:

Comply with classification standards and seek professional advice if uncertain.

14. Overclaiming Tax Credits

However, tax credits can be advantageous; however, improperly claiming tax credits – particularly refundable tax credits – could result in an audit.

Frequent credits that attract attention:

- Earned Income Tax Credit (EITC)

- Research & Development (R&D) credit

Avoiding this risk:

- Check eligibility and keep proof.

15. Late Filing or Frequent Amendments

Consistently filing late or frequently amending returns can signal disorganization or potential inaccuracies.

How to avoid it:

File on time and ensure your return is accurate before submission.

Conclusion

The IRS Audit process need not be intimidating at all – unless, of course, you do not have your books in order. The causes behind most Audits tend to involve inconsistencies, inadequate record-keeping, and risky Tax management.

Proper accounting, compliance with tax regulations, and expert advice will help minimize your exposure.

FAQs

1. What causes the IRS audit most of all?

Unreported income, unusual deductions, discrepancies in financial statements, and regular business losses are typical reasons that cause an IRS audit since the agency employs Automation to identify any suspicious data.

2. Is deduction usage a risk factor for getting an IRS audit?

It is not. Deduction is an integral part of tax accounting since it allows a taxpayer to save money. Excessive or inappropriate deductions, however, depending on the income levels, can be suspicious enough to cause additional investigation.

3. Is it easier to audit a large or a small business?

While it is possible to audit both, a small enterprise that operates through cash transactions is more prone to IRS investigations than others.

4. How long ago can the IRS audit a tax return?

In general, the IRS audits only returns submitted no later than three years ago. If the agency doubts about income reporting, the limit can be up to six years.

5. What does the IRS do if it detects a mistake?

Depending on the severity, it requires you to pay extra money and penalties. In extreme situations, there may be legal consequences.

6. Is there any way I could avoid being audited by the IRS?

Although there is nothing that guarantees that you won’t be audited, keeping good record-keeping practices and filing accurate returns greatly decrease your risk.

7. How do I respond if I’m audited?

Keep your cool, prepare all necessary documents, and even seek the help of a tax professional.